Scenario planning

Scenario planning attempts to take into account the many things that could happen and from those to build a number of believable, alternative futures. Not all the events that could happen are likely to happen together, so those permutations can be eliminated. For example, if an election is likely and we believe that a change in government would lead to a cut in public spending and a drop in interest rates, then there is no point considering a scenario of the new government reducing public expenditure and increasing interest rates as that is an implausible scenario. This greatly helps to reduce the number of ‘universes’ we have to consider and allows the organisation to concentrate on the few most likely ones and plan its response to each of the plausible scenarios.

Sensitivity analysis

Investigate the effect of assumptions about the future changing. Investigate sensitive assumptions more to get greater assurance. Look for ways of defusing high risk areas.

Decision trees

Decision trees can be used to map out the various patterns of events that can occur. Expected values can be used to evaluate the possibilities, or if probabilities are too difficult to estimate, the possibilities can be examined under conditions of uncertainty.

Note, however, that although expected values are often calculated, this approach to strategic planning is almost always inappropriate. Expected value calculations reduce detail into a single figure, that is usually not ‘expected’ to occur, and this is the reverse of what is required to encourage responsiveness, robustness and resilience. All of these require attention to detail.

For example, Quandary Co could spend $8m and then either have earnings of $20m with a probability of 0.6 or could make a loss of $5m with a probability of 0.4. Let us assume that the project lasts 10 years and that all financial flows are in present value terms.

The expected value of this project is:

-8 + 0.6 x 20 + 0.4 x (-5) = $2m

However, this positive result conceals the 40% chance that the company will have an adverse cash flow of $13m ($8m cost and then a $5m loss). Often, that type of adverse outcome could lead an organisation into liquidation, so ignoring the downside risk (and there might also be additional unknown ones) is certainly not a robust methodology.

Furthermore, this approach, as presented, does not show responsiveness or resilience. Cash flows and probabilities are both subject to change and the company seems to be signing up to a 10-year project that is all or nothing. Although sometimes the nature of a project will mean there is little or no flexibility, it is beholden on companies to look for flexibility.

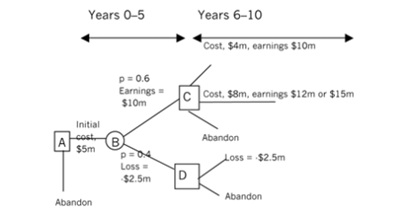

Now assume that further investigation shows that the project can be broken down into two, consecutive five-year blocks. The initial cost will be $5m and this will generate half of the original amounts: either a profit of $10m or a loss of $2.5m. Assume that after the first five years have passed, the company will have gained information that allows it to predict with certainty what the outcomes of the second five years will be. This is not unreasonable as the passage of time allows more information to be collected that can be used for further analysis. Also, events that had been a long way off are now closer and easier to predict. Therefore, the income figures shown below for the second five years are not known at the outset but are known after the first five years.

If the company wants to continue after five years, expenditure of another $4m will be needed to generate the same earnings as would have been earned with the original one-stage investment ($3m to bring the cost up to the original $8m plus a premium of $1m for the delay).

Alternatively, enhancement expenditure of $8m would then increase earnings to $12m or $15m depending on the state of the world economies (this will be known after five years). This possibility wasn’t even suspected at the very start of the project, but has now opened up.

If Quandary didn’t wish to invest further funds after five years, the project could be abandoned at the end of the first five years for no further cost. If the outcome had been poor in the first five years, it will be poor in the second five also, irrespective of any attempt at enhancement.

The choices and outcomes are now:

The company’s game plan could now be as follows:

1. Assess the likely outcomes from the first five years. As far as has been forecast, this will either be a net profit of $5m (10 – 5) or a loss of $7.5m (-2.5 -5). The expected value of the first five years alone would result in break-even (0.6 x 5 – 0.4 x 7.5 = 0). Within that figure there is a high chance the loss will occur and the company should have a good hard look at whether it is robust enough to stand a loss of $7.5m (plus a bit more for headroom).

2. If Quandary Co embarks on the project and makes a loss in the first five years, then, to avoid further loss, the project can be abandoned. This option provides responsiveness.

3. If Quandary Co embarks on the project and makes a profit in the first five years, the company can reassess what it should do then. Its choices are:

- abandon the project. This could be done if the economy then looked very poor so that the company didn’t want to risk a further $4m or didn’t feel robust enough to do so

- spend $4m to earn $10m; a profit of $6m

- spend $8m in the hope of earning either $12m or $15m; profits of $4m or $7m. (The company would, in fact, presumably not spend $8m to earn $12m because that profit of $4m is less than the profit of $6m that the first option gives.)

These provide responsiveness and also resilience because Quandary Co has been able plan to spend to rebound if economies improve.

Of course, as it turned out, none of these happened. A black swan was sucked into the cooling inlet pipe of the local nuclear power station causing a meltdown of the core. All homes and businesses, including Quandary Co, within a radius of 20 km had to be abandoned.

Ken Garrett is a freelance lecturer and writer

References

(1) The Black Swan, Taleb NN, Penguin, 2010

(2) Chaotics, Kotler and Caslione, Chaotics, Amacom, 2009